Lessons From History

The seriousness of the Covid 19 pandemic cannot be understated; but, there are lesson to be observed from the last major pandemic to impact the Australian continent. The Spanish Flu emerged in Europe over the closing days of the First World War. By 1919, the Spanish Flu had arrived in Australia. The last web reference is an outbreak in Cairns in December 1920. World- wide , estimates claim some 50-100 million people died. In Australia, estimates suggest that 15 000 people were dead within twelve months. Clearly, the Spanish flu impacted substantially upon the Australian economy and its social fabric.

Whilst policies varied amongst the States, governments were active in combatting the pandemic. State borders were closed. There were closures also of schools, churches, theatres, hotels, sporting activities, and country shows. From the web at least one state, NSW, seems to have compensated businesses affected by policies. Like now though, there appears to have been confusion and uncertainty surrounding policy application and delivery. This time, a national cabinet has been formed to develop and implement policies that have closed State borders, shut down non-essential industries, closed sporting events, theatres, restaurants, pubs, and district shows.

A major policy question that must occupy political debate is how expenditure policies can be funded to support expected economic contraction as unemployment rises, businesses close, bankruptcies occur, asset value collapse and savings evaporate. The social fabric of society also erodes as economic contraction gathers momentum. Public expenditure becomes necessary to stabilise economic contraction where possible and soften the impact of “moth balling” the economy.

One thing seems clear is that the duration of this pandemic will not be short. The “moth-balling” of the economy has no precedent in economic literature; but, a rapidly rising national debt is inevitable as cost of applied policies mount. This short discussion looks at the experience of the Spanish flu, Great Depression, and Second World War to demonstrate that a theoretical solution lies in economic growth.

Economic Contraction Inevitable.

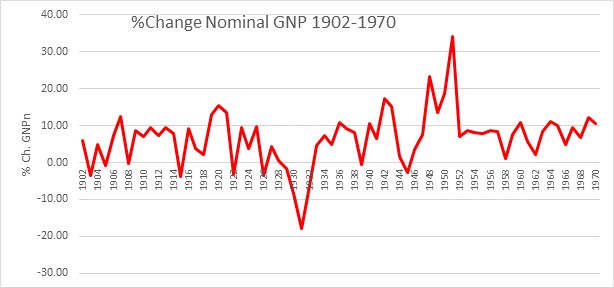

Chart 1

The Spanish flu era shows empirically GNPn began contracting from 1920. From 1921 to 1922, the economy goes into free fall bottoming out at -3.34%. Over 1920-22 nominal GNP in Australia contracted 17.8%. This severe economic contraction remains unexplained in economic literature, but, circumstantial evidence would identify the Spanish flu factor. Over 1919-20, it is estimated that the flu caused 15, 000 deaths or approximately 3% of the Australian population. Under such circumstances, government expenditure became necessary to stabilise both the economy and the social fabric.

Similarly, Covid -19 policy response in 2020 is to throw money at every contingency that arises or is anticipated. Already, a debate over funding applied policy is emerging amongst the political class and media “experts”. For example, taxes must rise to pay for policies otherwise future generations shoulder the responsibility for the rise in national debt. Another school of thought argues that austerity policies will be necessary to bring budgets back into balance. The focus upon balancing the budget amongst media “experts” and political commentators reflects the abysmal level of economic knowledge of modern times.

Meanwhile as policies shut down industries unemployment rises, businesses close, rental impost mount, life savings vanish. Home foreclosures become inevitable as finance houses move to protect asset portfolios wreaking further economic dislocation. This short discussion attempts to bring some theoretical perspective upon the national debt debate that must arise

National Debt and Economic Growth

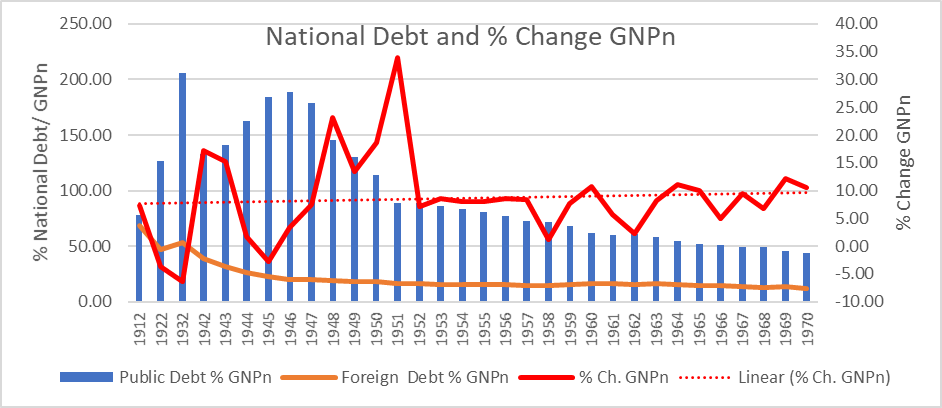

Chart 2.

1. National Debt comprises both State and Commonwealth debt

2. National Debt data prior to 1942 is at ten year intervals.

In public finance theory, national debt can be managed through economic growth provided two principles pertain.

- Growth in debt must be less than growth in GDP

- National debt should be raised domestically

Raised domestically, national debt contributes to economic growth in two ways. Firstly, public borrowings build both infrastructure and the industrial base of the nation. Secondly, Interest on national debt paid to risk averse domestic investors becomes personal income which is taxed; but also, stimulates economic growth when spent. Political objections demanding future austerity policies to balance budgets; and generational burdens do not withstand theoretical analysis

Chart 2 shows empirically the relationship between national debt and economic growth from Federation to 1970. Over time, an increase in national debt has been necessary to support economic growth in times of severe economic dislocation. External shocks to the Australian economy are identifiable as severe economic contractions: pandemic of 1922, the Great Depression, and, World War II. These external shocks severely impacted upon domestic economic growth and required expansive government expenditure to support the economic system.

For example, the severe economic contraction over 1920-22, resulted in national debt rising to 126.8% of GNPn. Within a decade the Great Depression required government expenditure to support the economy which lifted debt to 206% of GNPn. In 1939, Australia became involved in the second World War. The Australian War effort funded by national debt peaked at 188% of GNP in 1946. Strong economic growth under the economics of Keynes reduced national debt to 89% of GNPn by 1951. Moreover, in 1949, the Snowy Mountains Scheme began construction.

Once Australia had recovered from the volatility of wartime expenditure demands, the trend line through GDPn (1952-1970) demonstrates ability of stable and rising economic growth to manage and reduce the impost of national debt upon GNPn. National debt fell from 88% of GNPn in 1952 to 44% by 1970. Today’s political class would be horrified at those historic levels of national debt; and, terrified at what international ratings agencies might think about Australia’s financial risk profile. Historically though, the positive role of economic growth upon national debt is undeniable.

Australian External Accounts

A major difficulty in the Great Depression was public foreign debt. Australia had borrowed overseas and used the funds to build social infrastructure such as schools of art. When the Depression hit the economy, those social investments contributed no income; and, foreign debt became a dead weight upon a distressed economy. Compare foreign debt in 1932 at 53% of GNPn with the 2018 sum of both public and private foreign debt equalling 57.1% of GDP. Given the impact of Covid-19 upon the economy, the value of the $AUD must depreciate compounding the dollar value of external debt upon a contracting economy. It seems history has not taught our financial “experts” and monetary managers anything. External debt must become a real policy problem as Covid-19 progresses.

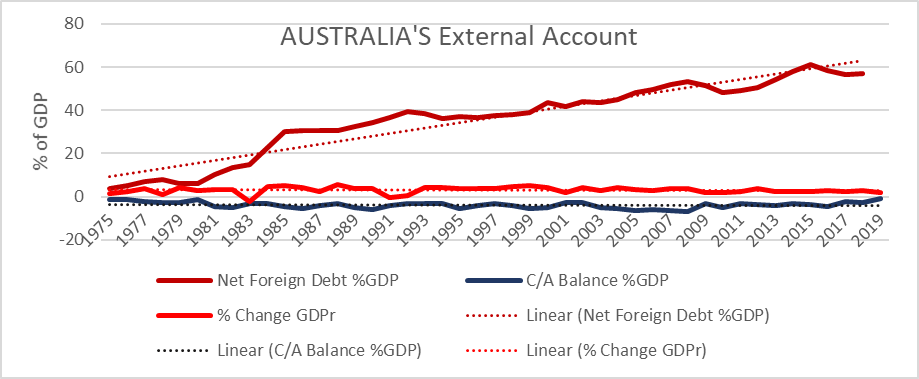

Chart 3

Chart 3 comprises three important long term curves from 1975 to 2019: external debt as a percentage of GDP; economic growth, and net income flow as a percentage of GDP. Net income flow comprises net interest payments on foreign debt plus net dividend flows on foreign investments. From RBA online Statistical Tables, June 2019, net debt payment was 4.6% of GDP whilst net income deficit was 2.9% of GDP. The net income flow identifies as a percentage of GDP the real costs of overseas borrowing and foreign investments in Australia. The significance of the net income deficit is that the Australian economy must grow at a greater rate than 2.9% before domestic growth is calculated. Given the disappointing rates of economic growth under global monetarism particularly since 2007, that will be a big ask.

Conclusions:

- Twenty years of tepid economic growth has come to characterise global monetarism. National debt levels that must inevitably accompany Covid -19 policy positions will require much stronger economic growth rates than achieved under global monetarism. A rethink of underlying economic philosophy will be critical to future economic and political stability.

- Post 1983 economic structural reforms have narrowed the production base of the economy. International closure of borders has exposed the inability of the Australian economy to be self- reliant in difficult times. A sound industrial policy to rebuild our depleted industrial base will be critical for long term stability. The real legacy of the Cairns Group of free traders is now exposed

- The hallmark of monetarism over the 1980’s and early 1990’s was an independent central bank. Independence was granted to the RBA in 1996. As monetarist rely on the natural rate of unemployment to manage price stability, the level of aggregate demand, and the exchange rate, reliance upon one main policy instrument breaches Tinbergen’s Rule of one policy instrument per economic target. The role of the RBA must be reviewed

- As the pandemic bites, the Australian Government will need to reclaim control of monetary policy and re-evaluate our exchange rate regime.

END

About Ben Rees B. Econ.; M. Litt. (econ.)

Economist, Farmer, Researcher, public speaker.

Import Replacement. An Option For Economic Recovery

The proposition that “the time for new ideas has arrived“, is highlighted by the Federal Coalition Government, now advocating deficit spending to achieve higher economic activity and ultimately employment. They are even asserting higher employment is required to lift wages, yet they have been through time, perhaps the most vociferous advocates of austerity and wage

Read more

The Making of History

I am a recent user of Twitter, and I have enjoyed the discourse therein, I noted the ABC radio announcer Steve Austin had made a comment about an article; it was rather strong for Steve I thought. That article written by Rutger Bregman; https://thecorrespondent.com/466/the-neoliberal-era-is-ending-what-comes-next/61655148676-a00ee89a carefully articulates the back-story of government changed, and we saw the

Read more

Toward a Stable Farm Sector – Multi Peril Insurance

Farmers First began life with the intention of facilitating the delivery of a Multi Peril Insurance product for the cropping sector around Australia, and once bedded down, rolling it out to other cropping and then livestock industries. Most of the rest of the developed and even developing world has this insurance cover, and in many

Read more